Skip to content

Skip to content

Haulage insurance is a type of commercial insurance that protects haulage businesses, drivers, vehicles, and transported goods against financial losses arising from accidents, theft, damage, liability claims, and other risks associated with road freight transportation. Coverage is available through a range of policy types, including haulage business insurance, contractor insurance, hauliers’ liability insurance, fleet insurance, cargo and freight insurance, public liability insurance, and commercial haulage insurance. Together, these policies help businesses manage risks associated with vehicles, cargo, employees, and third parties while meeting legal and contractual obligations.

In addition to covering vehicle damage, goods in transit, third-party injury, property damage, theft, fire, legal expenses, and European operations, haulage insurance requirements are influenced by factors such as the type of goods transported, fleet composition, claims history, liability needs, and supply chain complexity. As a result, businesses should assess their operational risks carefully when selecting coverage. Choosing the right insurance provider and policy structure helps ensure regulatory compliance, financial protection, and long-term business continuity across local, national, and international transport operations.

Why is Haulage Insurance Important?

Haulage insurance is important because it protects haulage businesses and HGV (Heavy Goods Vehicle) operators from the financial, legal, and operational risks associated with transporting goods. It helps businesses manage unexpected events such as accidents, theft, cargo damage, and liability claims while supporting regulatory compliance and maintaining uninterrupted transport operations.

Key reasons haulage insurance is important include:

- Protection Against Cargo Loss and Damage: Provides financial cover if goods are lost, damaged, or stolen while being transported by HGVs and other commercial vehicles.

- Coverage for HGV Accidents: Helps cover vehicle repair costs, replacement expenses, and other losses resulting from road accidents involving commercial freight vehicles.

- Third-Party Liability Protection: Covers claims involving injury to third parties or damage to their property caused by haulage operations or HGV use.

- Legal and Regulatory Compliance: Helps haulage companies and HGV operators meet insurance requirements necessary for operating commercial vehicles on public roads.

- Financial Security: Reduces the financial impact of unexpected incidents and helps protect business cash flow.

- Operational Continuity: Supports faster recovery from disruptions, allowing HGV fleets and delivery operations to continue with minimal interruption.

What Types of Haulage Insurance Are Available?

The types of haulage insurance available include haulage business insurance, haulage contractor insurance, hauliers’ liability insurance, and haulage fleet insurance. Other options include light haulage insurance, cargo and freight insurance, public liability insurance for haulage, and commercial vehicle and lorry insurance. Businesses can also choose logistics and transport insurance, carriage of goods for hire and reward insurance, and commercial haulage insurance, depending on their operational requirements and level of risk exposure.

11 types of haulage insurance are:

- Haulage Business Insurance

- Haulage Contractor Insurance

- Hauliers Liability Insurance

- Haulage Fleet Insurance

- Light Haulage Insurance

- Cargo and Freight Insurance

- Public Liability Insurance for Haulage

- Commercial Vehicle and Lorry Insurance

- Logistics and Transport Insurance

- Carriage of Goods for Hire and Reward

- Commercial Haulage Insurance

Haulage Business Insurance

Haulage business insurance is a comprehensive policy designed for companies that transport goods by road. It protects against common risks such as vehicle damage, cargo loss, theft, accidents, and third-party liability claims, helping businesses reduce financial exposure and maintain smooth operations. This cover is commonly used by haulage operators, fleet owners, and logistics providers. Policies include vehicle insurance, goods-in-transit cover, and liability protection, although exclusions may apply to uninsured cargo, unauthorised vehicle use, or losses caused by driver negligence. By covering multiple operational risks, haulage business insurance supports regulatory compliance, business continuity, and effective risk management.

Haulage Contractor Insurance

Haulage contractor insurance is intended for independent haulage contractors who transport goods on behalf of clients. It offers financial protection against operational risks such as vehicle damage, cargo loss, theft, and liability claims arising from accidents or property damage. This insurance covers commercial vehicles, goods in transit, personal liability, and contractual obligations related to haulage work. Certain risks, including employer liability and fleet-wide protection, are covered under separate policies. This insurance helps contractors manage business risks, meet legal obligations, and safeguard their operations against unexpected financial losses.

Hauliers Liability Insurance

Protecting customer goods during transit is the primary purpose of hauliers’ liability insurance. It covers a haulier’s legal responsibility for third-party cargo that is lost, stolen, or damaged while being transported. Cover may include compensation for goods affected by accidents, theft, or handling incidents, helping businesses manage the financial risks associated with carrying client freight. This protection can also help maintain customer confidence by demonstrating financial responsibility when transporting valuable goods. By reducing exposure to costly cargo-related claims and supporting contractual obligations, hauliers’ liability insurance forms an essential part of a comprehensive haulage insurance strategy.

Haulage Fleet Insurance

Haulage fleet insurance is a specialist policy that covers multiple commercial vehicles used within a haulage business. It enables operators to insure their trucks and vans under one agreement, creating a more streamlined approach to fleet protection. The policy covers risks such as accidents, theft, vehicle damage, and third-party liability, providing consistent protection across the fleet. It also helps businesses improve policy administration, maintain compliance, and manage financial exposure associated with vehicle-related incidents. For haulage companies that rely on several vehicles, fleet insurance forms an important part of a comprehensive risk management strategy.

Light Haulage Insurance

Light haulage insurance covers businesses and individuals that transport smaller loads using vans and light commercial vehicles. It is commonly used for local deliveries, courier services, and small-scale freight transport, where vehicle weights and cargo volumes fall below the requirements of heavy haulage. The policy provides cover for the vehicle, goods in transit, and third-party liability claims arising from accidents or damage during transportation. Addressing the specific risks associated with light freight operations helps operators maintain financial protection, manage risk effectively, and meet industry requirements. In contrast, light haulage insurance focuses on protecting smaller vehicles and their operations.

Cargo and Freight Insurance

Businesses that transport goods regularly rely on cargo and freight insurance to protect shipments against loss, theft, or damage during transit. Cover can apply to goods moved by road, rail, air, or sea and may include protection against accidental damage, theft in transit, and other unforeseen transportation risks. This insurance is commonly used by haulage companies, logistics providers, and freight forwarders, particularly when transporting high-value cargo or meeting contractual insurance requirements. By protecting goods throughout the transportation process, cargo and freight insurance helps reduce financial exposure and supports effective risk management.

Public Liability Insurance for Haulage

Public liability insurance for haulage protects businesses against third-party claims arising from injury or property damage linked to their haulage operations. This insurance cover addresses legal and financial risks when a haulage company’s activities cause harm to people or damage to property outside the business itself. Common scenarios include injuries to pedestrians near loading areas or property damage caused during loading and unloading activities. For example, if a haulage vehicle damages a client’s premises or a member of the public is injured due to haulage operations, public liability insurance can cover the resulting claims. This insurance helps haulage businesses meet legal obligations, manage liability risks, and protect their financial stability.

Commercial Vehicle and Lorry Insurance

Businesses that operate trucks, lorries, and other commercial vehicles rely on commercial vehicle and lorry insurance to protect their transport operations. This cover includes protection against vehicle damage caused by accidents, theft, fire, vandalism, and weather-related events, as well as third-party liability claims for injury or property damage. It may also include goods-in-transit cover to protect cargo during transportation. Operators of articulated lorries, rigid trucks, tippers, and refrigerated vehicles commonly use this insurance to reduce financial risk and safeguard essential business assets. By protecting vehicles and transport activities, this insurance helps businesses maintain compliance, minimise disruption, and keep deliveries moving efficiently.

Logistics and Transport Insurance

Logistics and transport insurance provides broad protection for businesses involved in transporting, storing, and distributing goods across the supply chain. It is commonly used by haulage companies, logistics providers, freight forwarders, and warehouse operators that manage multiple logistics functions. The policy covers loss or damage to goods, liability claims, and risks associated with warehousing, distribution, freight forwarding, and road transport activities. By covering several stages of the supply chain in a single insurance solution, logistics and transport insurance helps businesses manage risk, maintain operational continuity, and protect their financial interests across interconnected logistics operations.

Carriage of Goods for Hire and Reward

Operators who carry goods commercially on behalf of clients require carriage of goods for hire and reward insurance. It is a key part of commercial haulage operations, ensuring that operators have the appropriate cover to protect their vehicles, cargo, and liabilities when carrying goods commercially. This often includes goods in transit insurance, public liability insurance, and commercial vehicle insurance. These coverages help businesses meet legal and contractual requirements while reducing financial exposure to accidents, theft, cargo damage, and third-party claims. As a result, they provide essential protection for businesses involved in commercial haulage and B2B freight transport.

Commercial Haulage Insurance

Commercial haulage insurance is designed for businesses that transport goods on behalf of other companies as part of their freight and logistics operations. It provides protection for B2B haulage activities involving large freight volumes, high-value cargo, and long-distance or cross-border transportation. This insurance covers goods in transit, commercial vehicles, and liabilities arising from accidents, theft, or cargo damage. By protecting key business assets and addressing transport-related risks, commercial haulage insurance helps operators meet regulatory requirements, manage financial exposure, and maintain client confidence. It forms an important part of a comprehensive haulage insurance strategy for businesses involved in commercial freight transport.

How Does Haulage Insurance Work?

Haulage insurance works by providing financial protection when covered incidents affect vehicles, cargo, or haulage operations. After purchasing a policy, the haulage operator pays premiums, and the insurer covers eligible losses, damages, or liability claims in accordance with the policy terms and coverage limits.

The haulage insurance process follows these steps:

- The haulage business applies for insurance, and the insurer assesses factors such as vehicles, cargo types, routes, and operational risks.

- Based on this assessment, a policy is issued with specific coverage limits, terms, and premium costs.

- Once the policy is active, the business is protected against covered risks such as accidents, theft, cargo loss, or liability claims.

- If an insured incident occurs, a claim is submitted along with the required evidence and supporting documentation.

- The insurer then reviews the claim and verifies coverage under the policy terms.

- After approval, compensation is provided for eligible losses, helping the business recover financially and continue operations.

Who Needs Haulage Insurance?

Haulage insurance is needed for haulage companies, logistics providers, and businesses that transport goods by road using trucks, lorries, or other commercial vehicles as part of their operations. These organisations face risks such as cargo loss or damage, vehicle accidents, theft, and third-party liability claims. Under the Road Traffic Act, commercial cargo vehicles operating for Hire and Reward require valid motor insurance, and adequate cover is also required to obtain and operate an Operator’s License (O-license) in the UK. In addition, logistics hubs, warehouses, and clients frequently require proof of insurance before awarding contracts.

- Haulage Companies: Need haulage insurance to protect vehicles, cargo, and daily transport operations while meeting industry and regulatory requirements.

- Logistics Providers: Require haulage insurance to protect goods in transit and satisfy client, warehouse, and distribution partner insurance requirements.

- Owner-Operators and Haulage Contractors: Rely on haulage insurance to safeguard their vehicles, customer freight, and liabilities while transporting goods for payment.

- Businesses Transporting Their Own Goods: Benefit from haulage insurance by protecting commercial vehicles, equipment, and cargo against loss, damage, theft, and downtime.

- Fleet Operators: Depend on haulage insurance to reduce financial risk across multiple HGVs, drivers, and transported goods while maintaining uninterrupted operations.

What Does Haulage Insurance Cover?

Haulage insurance covers vehicle damage, goods in transit, third-party liabilities, theft, fire, breakdowns, legal expenses, and other risks associated with commercial transport operations. This protection helps haulage businesses manage financial losses, meet legal obligations, and maintain continuity when unexpected incidents affect their vehicles, cargo, or transport activities.

Key coverage of haulage insurance includes:

- Vehicle Damage: One of the main areas covered by haulage insurance is damage to vehicles resulting from accidents, collisions, fire, or vandalism. This protection helps cover repair costs or vehicle replacement when commercial vehicles sustain physical damage, allowing haulage businesses to maintain operational continuity and reduce financial disruption.

- Third-Party Injury: Haulage insurance also extends to third-party injury claims arising from transport-related incidents. As a result, businesses can manage compensation payments and legal liabilities when members of the public suffer injuries connected to haulage activities.

- Third-Party Property Damage: Damage to vehicles, buildings, loading bays, gates, fences, and public infrastructure can lead to costly claims, making haulage insurance essential for managing legal and financial responsibilities during transport operations.

- Goods in Transit: By safeguarding cargo against loss, theft, and accidental damage, businesses can protect shipment values and maintain customer confidence. Protection for goods in transit is a key part of haulage insurance cover.

- Public Liability: Claims arising from injury or property damage involving members of the public can also fall within haulage insurance cover. During loading, unloading, and delivery activities, this protection helps businesses manage the financial consequences of public liability claims.

- Employer’s Liability: Compensation payments, legal costs, and employer liabilities arising from employee injuries or work-related illnesses are covered under the employer’s liability section of haulage insurance. This protection helps businesses meet legal requirements and manage the financial impact of workplace-related claims.

- Breakdown Cover: Roadside assistance, vehicle recovery, towing services, and emergency repairs are covered under breakdown cover within a haulage insurance policy. These services help minimise vehicle downtime and support operational continuity when mechanical failures occur.

- Legal Expenses: Legal representation costs, defence expenses, regulatory matters, and certain contractual disputes can be covered under the legal expenses section of haulage insurance. Access to financial support for eligible legal costs helps businesses manage unexpected legal challenges.

- Theft and Fire: Financial losses resulting from vehicle theft, attempted theft, fire damage, and related incidents are covered under theft and fire protection within haulage insurance. This cover helps businesses recover from events that affect insured vehicles, equipment, and transport assets.

- European Cover: Selected haulage insurance benefits can be extended to vehicles and goods operating across European countries through European cover. This protection helps businesses maintain insurance coverage during international and cross-border transport activities.

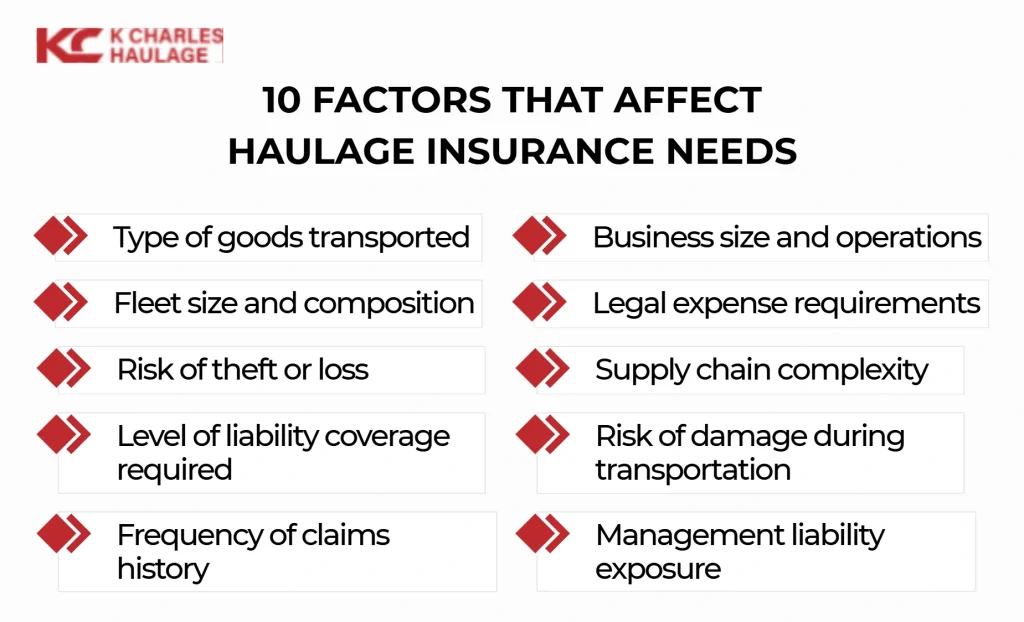

What Factors Affect Haulage Insurance Needs?

The factors that affect haulage insurance needs include the type of goods transported, fleet size, theft and damage risks, liability requirements, claims history, business operations, and supply chain complexity. These components influence the level of cover required, the risks a business faces, and the overall scope of protection needed to support safe and compliant haulage operations.

10 factors that affect haulage insurance needs are:

- Type of goods transported: Perishable products, hazardous materials, bulk commodities, and high-value items such as refrigerated food, chemicals, and electronics often influence policy conditions, coverage limits, and premium calculations. Different cargo types create different insurance requirements because the risks associated with transporting goods can vary significantly.

- Fleet size and composition: Businesses operating multiple lorries, vans, or refrigerated vehicles face greater operational complexity, prompting insurers to assess the number of vehicles and fleet composition when determining coverage requirements. Insurance needs often increase as fleets become larger or more diverse.

- Risk of theft or loss: Higher exposure to theft or cargo loss requires broader insurance coverage and stricter policy considerations. Factors such as high-value goods, unsecured parking locations, and high-risk transport routes can increase risk levels, while GPS tracking and secure storage measures can help reduce them.

- Level of liability coverage required: Contractual obligations, customer requirements, and legal responsibilities often determine whether higher or lower liability limits are needed to protect against third-party claims. The amount of liability protection a business requires plays a major role in shaping its haulage insurance policy.

- Frequency of claims history: Businesses with frequent claims may face higher premiums or stricter terms, whereas a strong claims record can support more favourable coverage conditions and insurer confidence. Past claims activity is often used as an indicator of future insurance risk.

- Business size and operations: Businesses with larger workforces, higher turnover, or wider operating areas often require more extensive haulage insurance cover. National and international transport operations face greater liability, vehicle, and cargo risks, which require broader coverage and higher policy limits.

- Legal expense requirements: Additional insurance protection is often required when haulage operations face exposure to legal disputes and regulatory matters. Legal expenses coverage helps manage the financial impact of claims, investigations, and contractual disagreements.

- Supply chain complexity: Greater supply chain complexity often increases haulage insurance requirements by creating more points of risk throughout the transportation process. Multiple suppliers, warehouses, distribution centres, and logistics partners can increase exposure to delays, cargo losses, and liability issues, necessitating broader insurance coverage.

- Risk of damage during transportation: Factors such as fragile cargo, adverse weather conditions, handling procedures, and road accidents can increase the risk of damage and influence coverage levels and policy terms. The likelihood of goods being damaged in transit plays a significant role in determining haulage insurance needs.

- Management liability exposure: Regulatory breaches, employment disputes, and allegations of mismanagement can expose directors and senior managers to legal claims and financial liabilities, making management liability cover an important consideration when assessing haulage insurance needs.

Does Insured Haulage Cost More?

Yes, insured haulage costs more than standard haulage because the transport provider assumes additional financial responsibility for the cargo being moved. The increased cost reflects the insurance coverage, which protects against risks such as theft, loss, damage, or accidents during transit. The exact price difference depends on factors such as cargo value, type of goods, transport distance, required coverage level, and overall shipment risk. While insured haulage involves a higher upfront cost, many businesses choose it to reduce potential financial losses and gain greater protection for valuable or sensitive cargo.

Should You Check Haulage Insurance Before Booking a Transport Service?

Yes, checking a haulage company’s insurance arrangements before booking a transport service helps determine whether sufficient insurance cover is in place to protect goods against damage, loss, theft, or accidents during transit. Businesses should verify the type of cover provided, whether goods in transit insurance applies, and any compensation limits or exclusions that affect their shipment. When booking transport services, businesses should always choose a fully insured haulage service that offers suitable protection for goods, vehicles, drivers, and third-party liabilities throughout the delivery process.